The Department of Commerce spent $11.2 billion on IT between FY2020 and FY2026 YTD. That number is misleading.

Commerce isn’t really one IT customer. It’s three different ones inside one department, with three different procurement personalities, three different vendor stacks, and three different growth trajectories. If you sell into “Commerce,” you’re selling into three different markets. Most vendors are only winning in one of them.

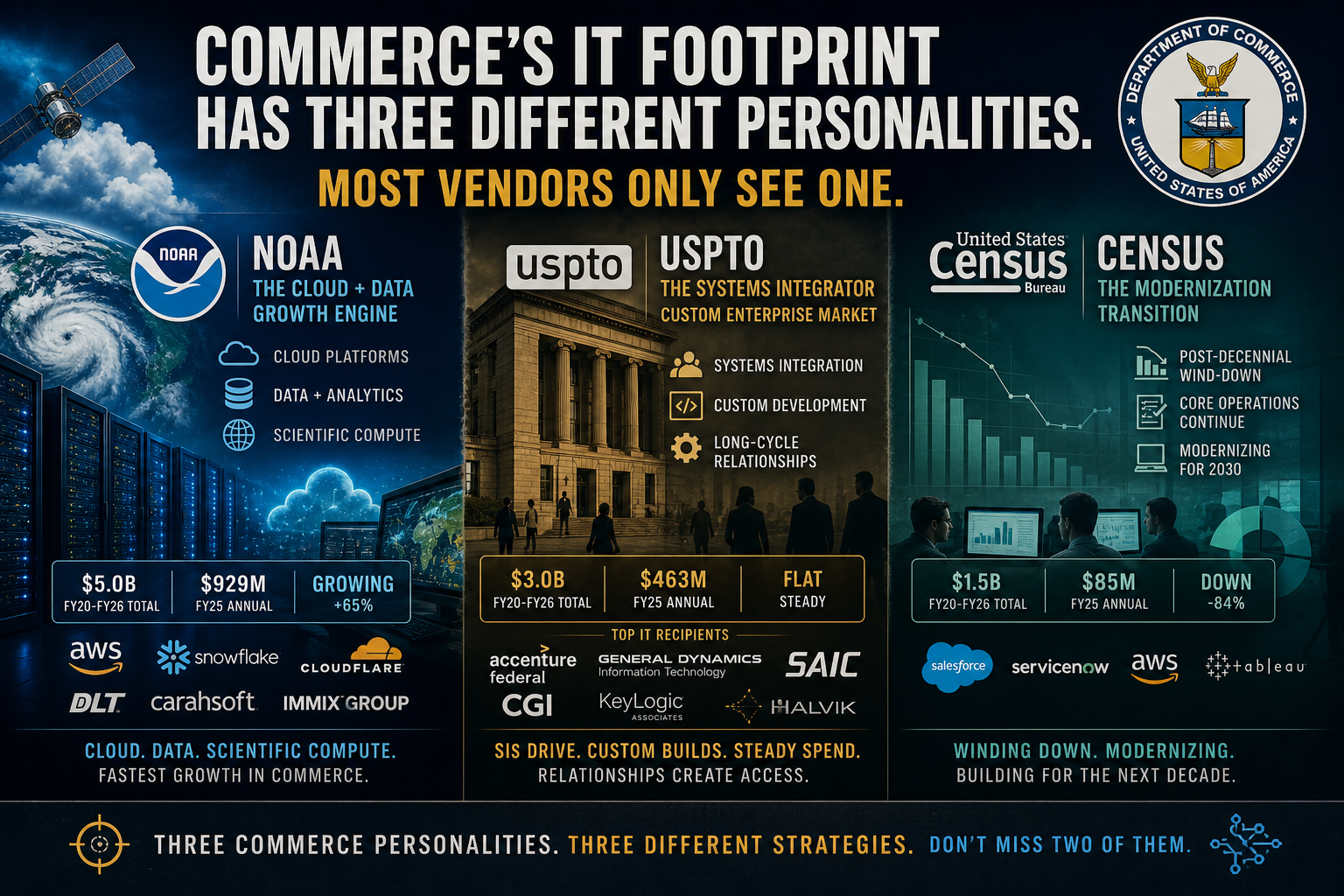

We pulled every Commerce IT transaction across FY20-FY26 and tracked spend by sub-agency, by vendor, by year. Here’s the actual shape of it.

The three Commerces

| Sub-agency | FY20-FY26 Total | FY25 Annual | Direction | Personality |

|---|---|---|---|---|

| NOAA | $5.0B | $929M | Growing 65% | Cloud + data + scientific compute |

| USPTO | $3.0B | $463M | Flat | Systems integrators + custom enterprise |

| Census | $1.5B | $85M | Down 84% | Post-decennial wind-down |

| Office of Secretary | $556M | $130M | Growing | Strategic / cross-cutting IT |

| NIST | $457M | $66M | Stable | Mid-size standards-driven IT |

| BEA | $39M | $7M | Stable | Statistical computing |

Three of those rows are doing very different things. The vendor patterns inside them confirm it.

NOAA is where the cloud action is

NOAA accounts for 45% of Commerce IT spend and is growing fastest. Annual NOAA IT went from $562M in FY20 to $929M in FY25 — up 65% in five years.

Where’s the growth concentrated? Cloud. Of $752M in cloud-related spending across all of Commerce since FY20, $484M (64%) flows through NOAA. Census is a distant second at $31M, NIST third at $25M.

This isn’t AWS direct buying. AWS shows up at $39M total Commerce-wide. The cloud volume comes through resellers — DLT, Carahsoft, ImmixGroup — handling AWS and Azure resold spend tied to NOAA’s geospatial and atmospheric workloads.

If you sell cloud-adjacent technology — observability, data platforms, edge compute, security tooling — NOAA is where the federal cloud opportunity is concentrated inside Commerce. Not “Commerce.”

USPTO is a systems integrator market

USPTO spent $3 billion on IT in the same period — second-largest sub-agency — and the vendor profile is completely different from NOAA’s.

The top six USPTO IT recipients are all systems integrators and consulting firms:

- Accenture Federal: $266M

- General Dynamics IT: $245M

- SAIC: $215M

- CGI Federal: $152M

- KeyLogic Associates: $144M

- Halvik: $123M

USPTO buys IT through long-cycle SI relationships supporting custom patent and trademark examination workflows. The product vendors (Microsoft at $71M, Dell at $63M, Oracle at $38M) are downstream of those SI relationships, not directly contracting.

If you sell hardware or software to USPTO without a relationship with one of those primes, you’re not really competing for USPTO business. You’re selling into whatever pull-through the SI decides to use.

Census is winding down — but not done

Census IT spend has dropped 84% from its FY20 peak ($524M) to FY25 ($85M). That’s the predictable post-decennial pattern: massive IT investment around the 2020 census, then steady decline through the inter-decennial years.

But it’s not zero. Census still ran $85M in IT spend in FY25 and is already at $36M in FY26 YTD — running infrastructure, doing intercensal surveys, modernizing for 2030.

The interesting wrinkle: Census’s vendor mix is starting to look like a modern enterprise stack. Salesforce, ServiceNow, AWS direct ($28M Census-wide), and Tableau all show up. The 2030 census is going to look very different from 2020 if these trajectories hold.

Vendor stories worth knowing

A few specific vendor patterns at Commerce:

Salesforce surged in FY23. Salesforce went from $11M in FY22 to $61M in FY23 across Commerce — most of that landing at NIST ($46M). The CRM modernization wave hit NIST specifically, and Salesforce captured it.

ServiceNow is now growing fast. Stable at $5M annually for years, then jumped to $18M in FY25 and is already at $16M in FY26 YTD. ServiceNow appears to be winning workflow modernization across multiple Commerce sub-agencies simultaneously.

Cisco is shrinking. $23M in FY20, $10M in FY25 — down 55%, the same on-prem-network compression we saw at USDA. NOAA is shrinking Cisco fastest as workloads migrate.

Dell is the steady giant. $407M total over six years, the largest individually-classified vendor across Commerce. Dell’s volume holds steady because the systems integrators serving USPTO and the cloud reseller channels at NOAA both pull through Dell hardware.

Palantir appeared. $8.4M total, mostly at the Office of the Secretary. New entrant, growing.

The takeaway

Three things hold across the data:

- One Commerce strategy doesn’t work. A vendor with strong NOAA traction and no USPTO relationship is positioned for half the market. A vendor strong at USPTO and absent from NOAA’s cloud growth is positioned for the half that’s flat.

- End-user attribution beats awarding office every time. Office of the Secretary issues many of the largest contracts, but the actual technology consumption is at NOAA, USPTO, Census, and NIST. Funding agency tells you who’s actually using the technology.

- The fastest-growing dollar segment in Commerce IT is cloud at NOAA. Anyone treating Commerce as a flat $11B market is missing where the budget is actually moving.

What’s next

We’ll publish the SSA breakdown next, then DOE national laboratories — where the procurement dynamics are even more unusual.

If you sell into Commerce and you’re operating from a flat agency view, the most useful question to ask this quarter: which of the three Commerces are we actually winning, and which are we missing? The answer almost certainly isn’t what your CRM dashboard shows.